Franchising is the most underrated economic technology

Across retail, food, and services, the same tension keeps resurfacing. Do we preserve small, independent businesses, even if that means informality, lower quality, and weaker productivity? Or do we modernize aggressively, accepting that larger, more structured companies will absorb market share and gradually squeeze out the middle class of small business owners?

This dilemma is usually presented as binary. But there is a path that reconciles modernization with local ownership, and efficiency with social stability. It’s called franchising, not as branding, but as a production system.

For the average snack shop or neighborhood pizzeria, reinventing recipes, sourcing, and supplier negotiations almost always leads to mediocre outcomes. Franchising exists to absorb this complexity. It allows operators to start from a proven baseline: optimized recipes, negotiated supply chains, tested equipment, and predictable margins. It reallocates creativity away from low-leverage reinvention toward what matters: consistent operations.

Ownership without chaos

A franchise system does one thing exceptionally well: it separates ownership from standardization. Informality preserves ownership but loses standards. Corporate retail enforces standards but concentrates ownership. Franchising preserves ownership while enforcing standards. The franchisee owns a real business. The brand enforces consistency. This is how you modernize an economy without concentrating all value in a few hands.

The franchisee gains access to infrastructure they could never build on their own. The central entity provides scale advantages such as supply chain, technology, standards, sometimes the brand itself. The local operator contributes capital, labor, local knowledge, and day-to-day execution.

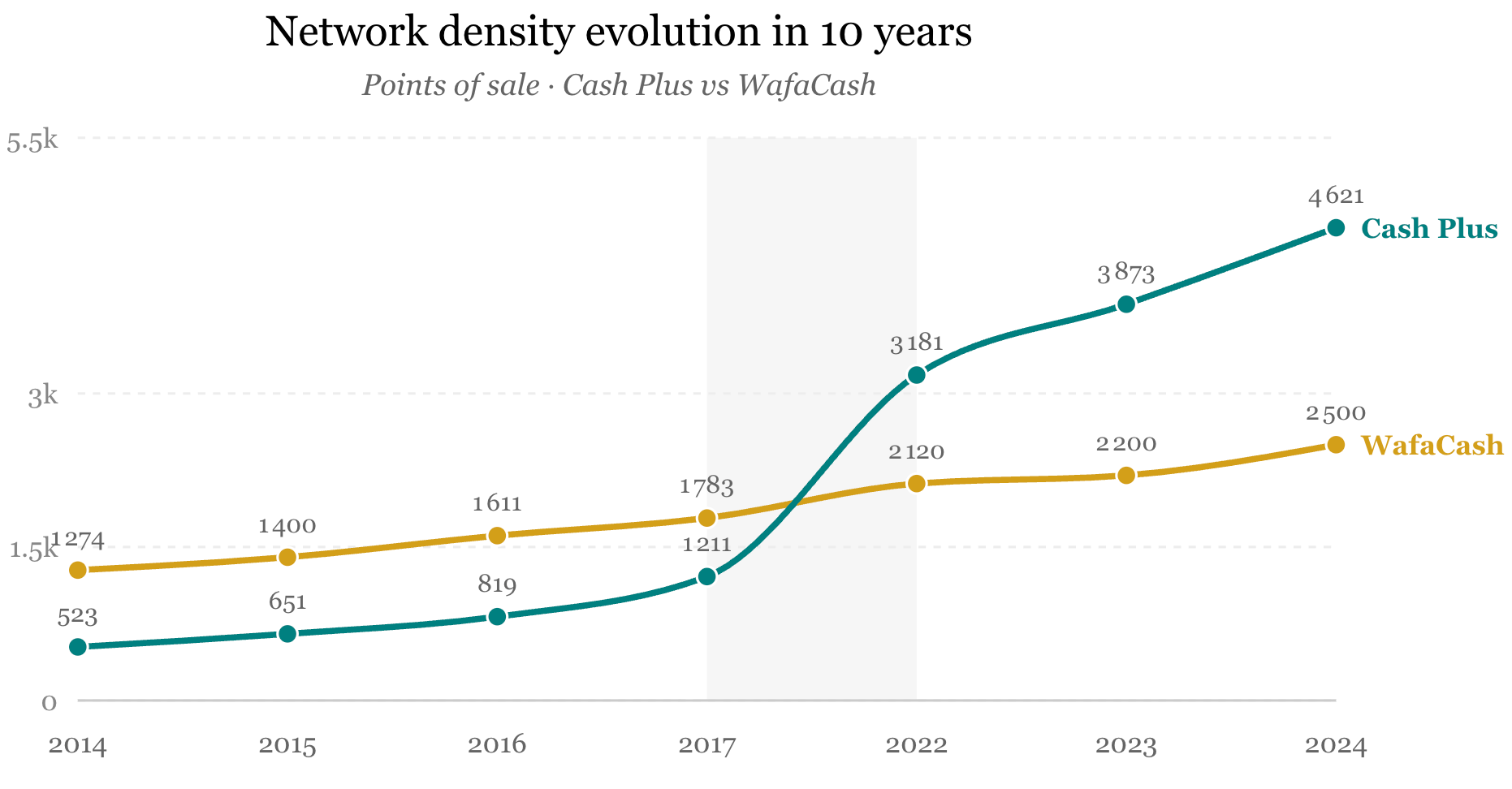

Study case: Morocco's largest franchise network

In Morocco, the clearest example is Cash Plus. With nearly 5,000 points of sale nationwide, it is today the largest franchise network in the country across all sectors.

Ten years ago, the situation looked very different. Wafacash was roughly two times larger than Cash Plus. Its network relied on a mix of directly owned stores and master franchises, requiring operators to run 20+ outlets to qualify. That overhead kills unit economics in rural areas and tier-three cities where demand is fragmented and margins are thin.

That left an opening. In this industry, network density and cost-to-serve are everything. Cash Plus solved both. Anyone could open a single franchise. Entry barriers are low: one shop, limited capital, and a commitment to operate within Cash Plus’s technology and compliance framework. The result was a fundamentally different incentive structure. Each franchisee had real skin in the game. Opening hours extend naturally. Service quality improves. If the owner is sick, the shop doesn’t close, a sister or cousin can step in. The real estate might belong to the family. Fixed costs are lower, and alignment is stronger than any employment contract could achieve.

Multiply this model by thousands of locations and something powerful emerges. Scale without bureaucracy. Coverage without overhead.

Franchising as centralization of the hardest problem

Every successful franchise is built on the same insight: most small businesses fail not because operators are bad, but because some problems are too complex or too expensive to solve at the unit level.

A good franchise centralizes one hard problem. It can be real estate, logistics, purchasing power, technology, cost-to-serve, or brand and standardizes it at the center. The local operator can focus on what actually matters: customers, staff, and daily execution.

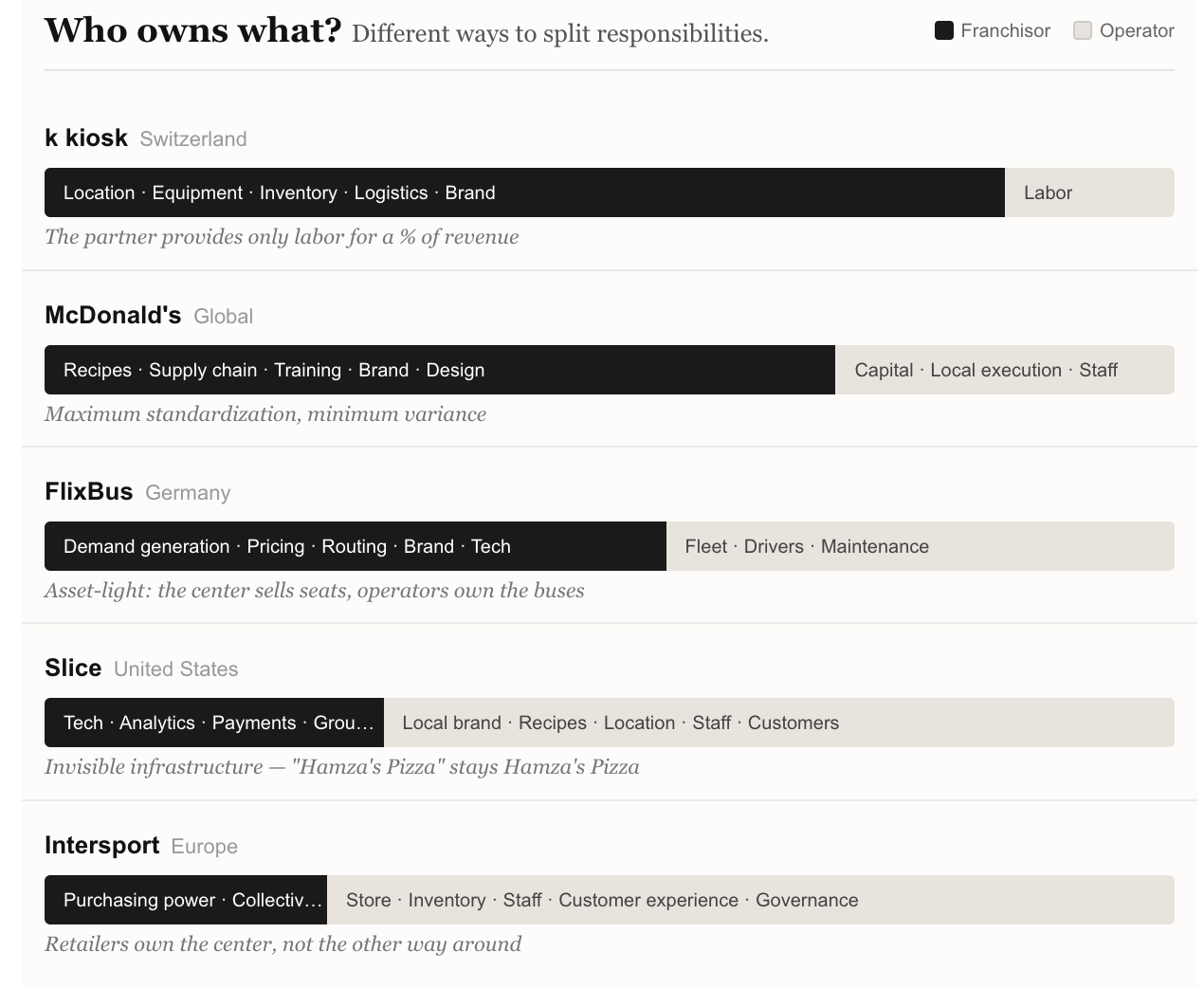

Franchise models vary widely in what gets centralized and who holds power. Some tightly control brand and experience; others operate as almost invisible infrastructure, centralizing assets, data, or purchasing while leaving identity and execution local.

The classical example is McDonald’s. Here, the franchisor centralizes almost the entire value chain: recipes, supply, training, branding, store design, and operations. The franchisee brings capital and local execution, but operates within tight parameters to ensure maximum standardization.

In Switzerland’s k kiosk model, the franchisor owns location, assortment, and logistics; the partner provides labor and execution for a revenue share. This is franchising reduced to pure execution. In a high-wage country like Switzerland, a fully corporate model would be costly as payroll and managerial overhead would explode, while incentives would remain weak.

At the other extreme sits Intersport, which flips governance. Independent sporting-goods retailers collectively own the brand. Their hard problem is purchasing power. Individually, a small mountain shop has no leverage against Nike or Adidas. Together, they negotiate on equal terms with global chains. Here, franchising is not about control from the center, but about collective scale.

Slice Pizza in the US represents perhaps the most invisible evolution of all. Slice does not ask pizzerias to rebrand. “Hamza’s Pizza” stays Hamza’s Pizza. Instead, Slice unbundles the franchise by centralizing technology, analytics, payments, and collective purchasing for boxes and ingredients. The hard problem here is software and scale. Slice builds once what no individual pizzeria could reasonably build alone.

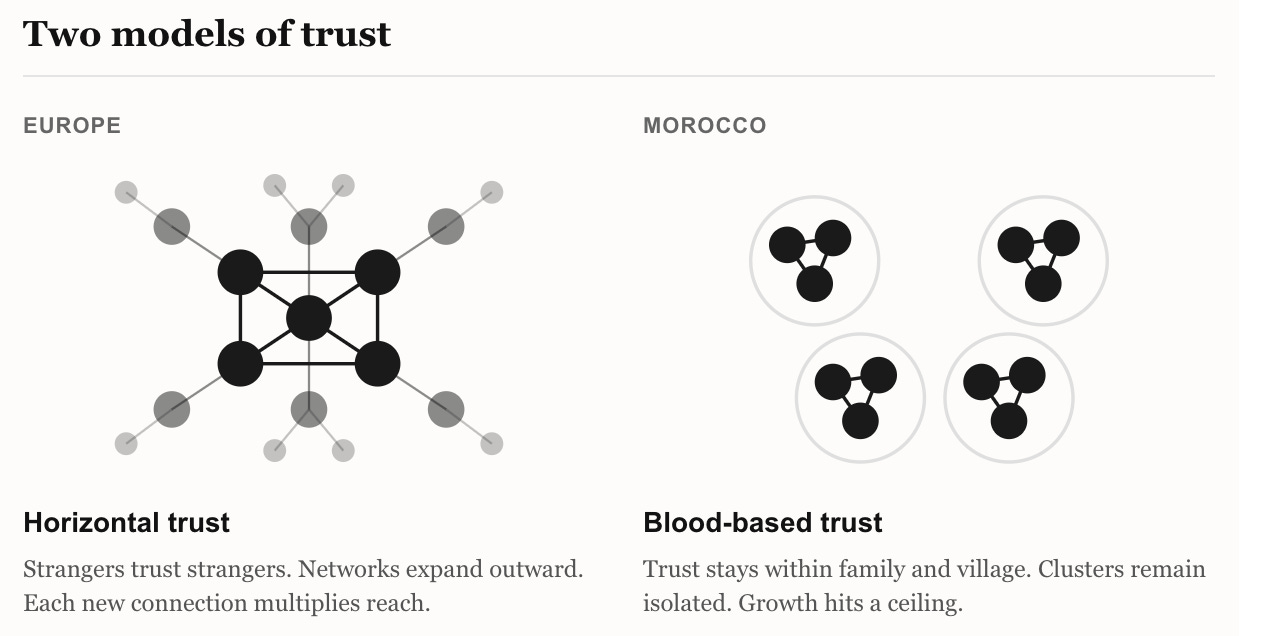

The Trust Problem: Why European Grocers Formed Cooperatives and Moroccan Didn’t

Why did small grocers in France and Germany build cooperative giants like Leclerc, Intermarché, or REWE, while Moroccan hanouts remained atomized for decades?

The answer is not ambition or intelligence. It is how trust, formality, and incentives interact. European cooperatives were built on horizontal trust: thousands of independent grocers, agreeing to pool capital and submit to collective rules. This was possible because France and Germany had centuries of mutual aid societies, and civic institutions that normalized cooperation among strangers.

Morocco’s social capital flows differently. Trust is blood-based: family, village, tribe. A shopkeeper trusts his cousin completely. He does not trust another grocer from a different city simply because they sell the same products.

European cooperatives were layered on top of already formal businesses. Shopkeepers had invoices, accounting, tax records, and enforceable contracts. Pooling purchasing power simply added scale to an existing structure. Most Moroccan hanouts are informal. No formal books, no VAT trail, no declared employees. This creates a rational disincentive. The efficiency gained from bulk purchasing (often single-digit percentages) is eclipsed by the cost of entering full formalization. Staying independent preserves an informality premium that cooperation would destroy.

A cooperative only works if members believe two things: that the center will not capture value unfairly, and that peers will not free-ride. That requires audits, sanctions, and fast dispute resolution. In high-trust environments, norms do much of this work. In lower-trust environments, it must be done formally. But, institutions often lack fast & reliable enforcement.

Closing thought

In every sector, the same question shows up: who owns the value chain, who bears the risk, and who captures the upside. In most emerging markets, that question is answered badly by default. Informality preserves ownership but kills scale. Corporate retail delivers scale but concentrates ownership. Franchising is the rare structure that refuses that trade-off.

The hardest problems move to the center. Ownership stays local. Morocco has dozens of sectors where that arbitrage hasn’t been captured yet. The question isn’t whether there’s room for more franchise networks. It’s who is going to build the center.